How Much Money Do You Need to Buy a House?

Many people think there are lots of hidden fees when buying a house and it’s often what holds them back from making any moves. In some ways, this is correct, but in reality it’s because there’s a lack of education around home buying. We are not taught this in school, and our parents bought at a very different time than we did. Things have changed!

Of course there will be “hidden” fees if no one is properly educating you on what to look out for!

We’re not about that - we want you to be empowered with all the knowledge you need to make a smart decision. So this is a super transparent and comprehensive guide on all the costs around buying a house!

Finished this article and want to learn more about the home buying process PLUS how to make that home an investment?

How much money do you need to buy a house?

When I first tried to buy a house, I thought you had to pay all cash. Truly, I thought you needed a briefcase full of money to slide across a conference table. I had no idea how it all worked! So it’s no surprise if you’re just starting to consider buying and you have zero clue what the process looks like (and for that, we’ve got a full first time buyer checklist).

Let’s break down the major costs that come with buying your first home:

Down Payment

The one you have likely heard of. Your down payment is the portion of the home price you need to provide at the get-go (the rest is covered by your loan). Although many people believe you need a 20% down payment on a home, that is not necessarily the case.

You may not need as much money up-front as you’d imagine!

20% is the amount you want to pay if you would like to avoid paying PMI (private mortgage insurance). However, when buying a primary residence you only really need 5% down, and 3% if it’s your first home purchase. Your PMI also automatically drops off when you hit 78% of the original property value. You may also request for it to be removed in the following situations:

the loan balance has fallen to 80% of the original property value

the loan balance has fallen to 75% of the appreciated value during years 2-5

the loan balance has fallen to 80% of appreciated value after year 5

Now before you start coming up with a number in your head of what you think you can afford - talk to a lender!

Once you find a great lender, they can assess your information and help you determine how much you could get approved for. They will even help you figure out if there is any way you could increase your financial situation to get the best rates and save you money in the long run.

You can also take the time to try and raise your credit score beforehand.

Closing Costs

You may have heard this phrase, but there is a good chance you have no clue what it really includes. Closing costs include all fees and charges that occur when officially transferring a property from one owner to another.

Some closing costs are paid by the seller and some by the buyer. Your closing costs are typically around 2-5% of the loan amount. Here are the closing costs you, as a buyer, would normally pay:

Application fee

Appraisal (sometimes separate, see next section)

Closing fee or escrow fee

Homeowners’ insurance

Mortgage Insurance

Title fees

Property Taxes

Etc

Inspection

Although home inspection isn’t technically required, you’d be crazy not to get one. A home inspection could potentially keep you from buying a money sucking property and save you thousands of dollars down the line. This inspection can also help determine if you want to require the seller to make some repairs before you buy.

Inspection costs depend on the size of the home you’re looking to purchase.

Inspection costs will vary depending on the size of a home. You can also add additional inspections outside of the standard, which would be for things like termites or detached structures like sheds or tiny homes.

For example, for a small home under 1,000 sqft, an inspection is normally around $300. A larger home, at about 3,500 sqft, is around $500. Again, these prices vary depending on your home size and city/state.

Appraisal:

As we previously mentioned, sometimes this is wrapped up in closing costs. But sometimes your lender will charge this outside of them.

If you are unaware, an appraisal is when a professional comes to determine the value of the home. This will help both you and the seller get a better idea of what the home is worth. If you’re in a hot market, you, as the buyer, may waive your appraisal addendum or have to pay some out of pocket fees.

The cost of an appraisal is also very different depending on where you live and the type of market you’re in. Typically, an appraisal costs anywhere from $400-$1,000.

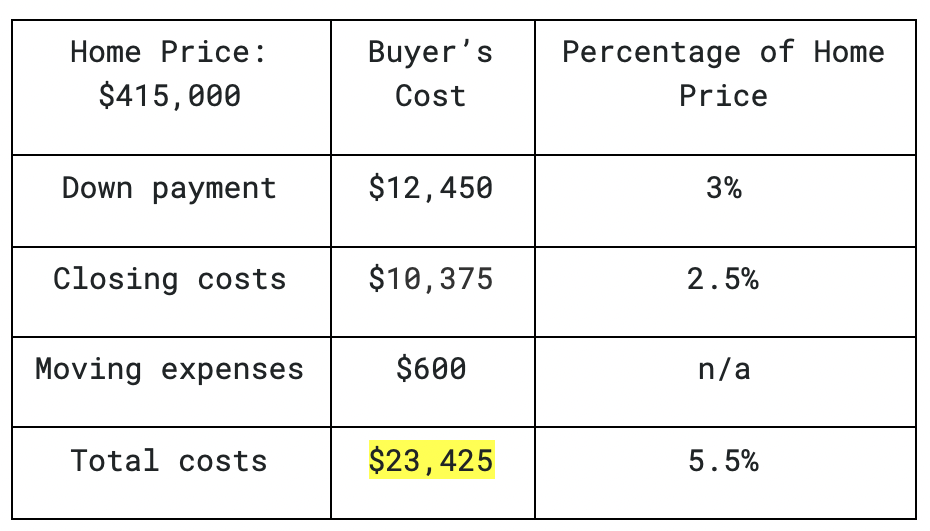

Real Life Example:

So now that we understand some of the fees, let’s look at a real life example:

home price: $415,000

*if the home sold for asking price

So based on the a list/sales price of $415,000, a downpayment of 3%, 2.5% closing costs, and $600 dollars in moving expenses, your total costs are $23,425! Again, these numbers could be different for you, depending on the area you live in. Now, time for the next question:

How Much Should You Save?

So it’s time to save for your costs to actually buy a house! Don’t forget to use that list above to figure out the amount you’ll have to save for upfront costs.

After this, it’s time to talk about reserves. How much money should you save if you want to buy a fixer upper or want to do work in your house, vs if you buy a move-in-ready home?

This truly depends on how extensive the work will be but a good rule of thumb we like to tell first time buyers is save 20% down payment and then plan to put 3% down and use the rest to reinvest into the house. We also recommend having around 2 mortgage payments extra as reserves on top of this because it’s better to be safe than sorry!

Now here’s one exciting thing that may make that looming number a little less scary: you may qualify for a first time homebuyer program!

If you use a Homebuyer Program you may need even less money! You may be able to qualify for one of these programs if you’re:

Military

Education

Fire Fighter

Have a lower income

Live in a certain area

etc

So how do you find one of these programs? Search for local grant programs in your specific city or state.

Your realtor should know of certain lenders who work with these programs, so make sure you’re aware and asking about the programs from the start of your search!

Real Life Example:

Now let’s see what it looks like when you buy with a first time buyer program! This person, let’s call them Sam, is a teacher and makes $40k a year. Sam worked with a lender who specialized in low income and education homebuyer programs.

If you really research your options, you can come out spending way less than you anticipated!

Sam made under $50K so they qualified for a certain grant program that covered the down payment. Sam then bought a house with a sales price of $265K.

Sam didn’t have to pay down payment, and only had to bring in $4K to closing! We know - amazing, right?!

You see, it’s really important to do your due diligence and find out what you can afford, and if you can get some sort of assistance to buy a home. Who knows, you may be ready and you didn’t even realize!

Are You Ready to Buy a House?

If you’re still sitting here wondering if you’re even ready to buy yet, then we’ve got the best solution for you: a quiz! Our quiz will let you know if the time is now, or if you need a little extra preparation.

Now even if it says you’re not ready, don’t fret! You are likely WAY closer than you may imagine. Along with your results, you’ll get actionable steps to make moves and make homeownership closer than you may have imagined. YOU GOT THIS!